Topic 1:EQUITY: OFF THE GUARD

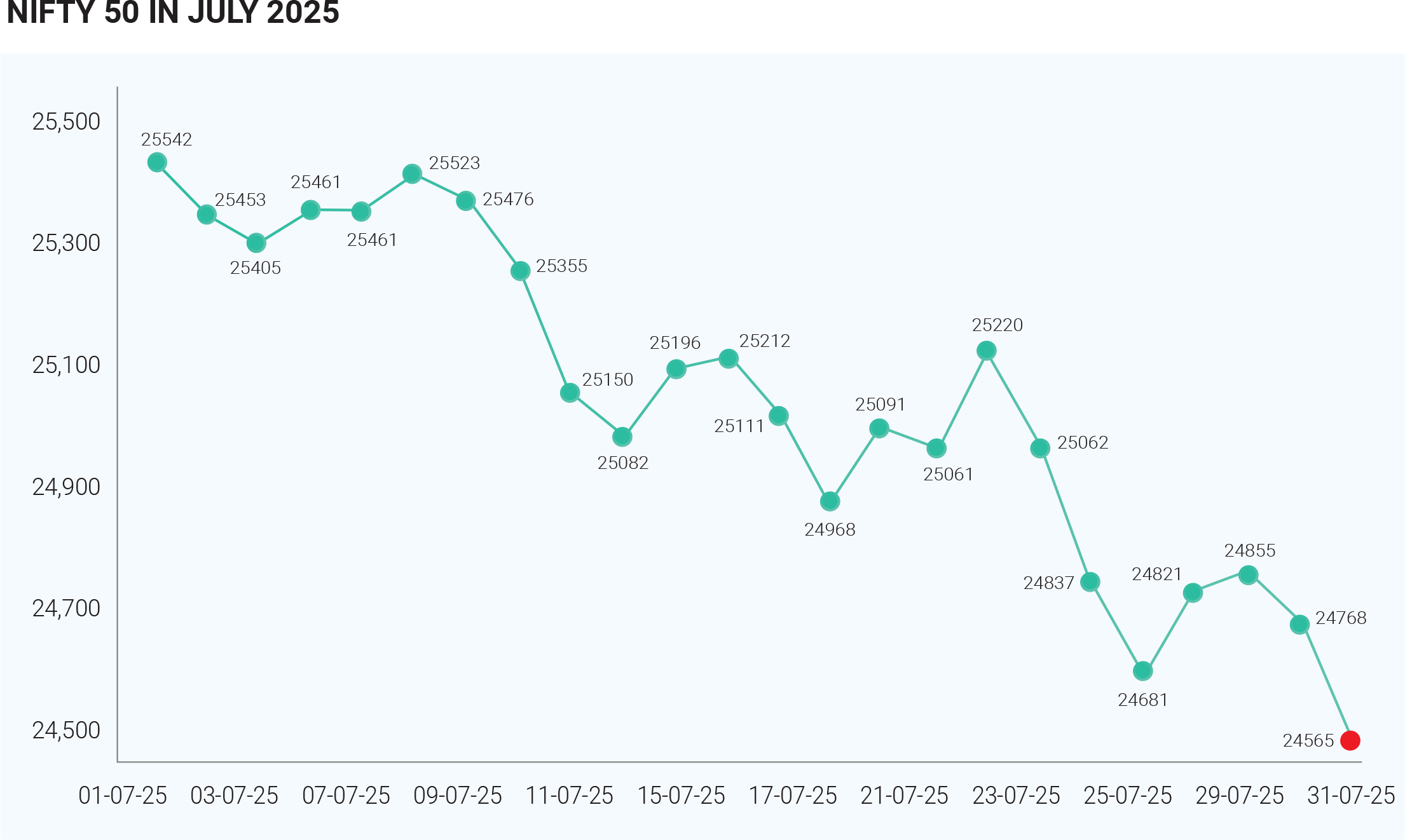

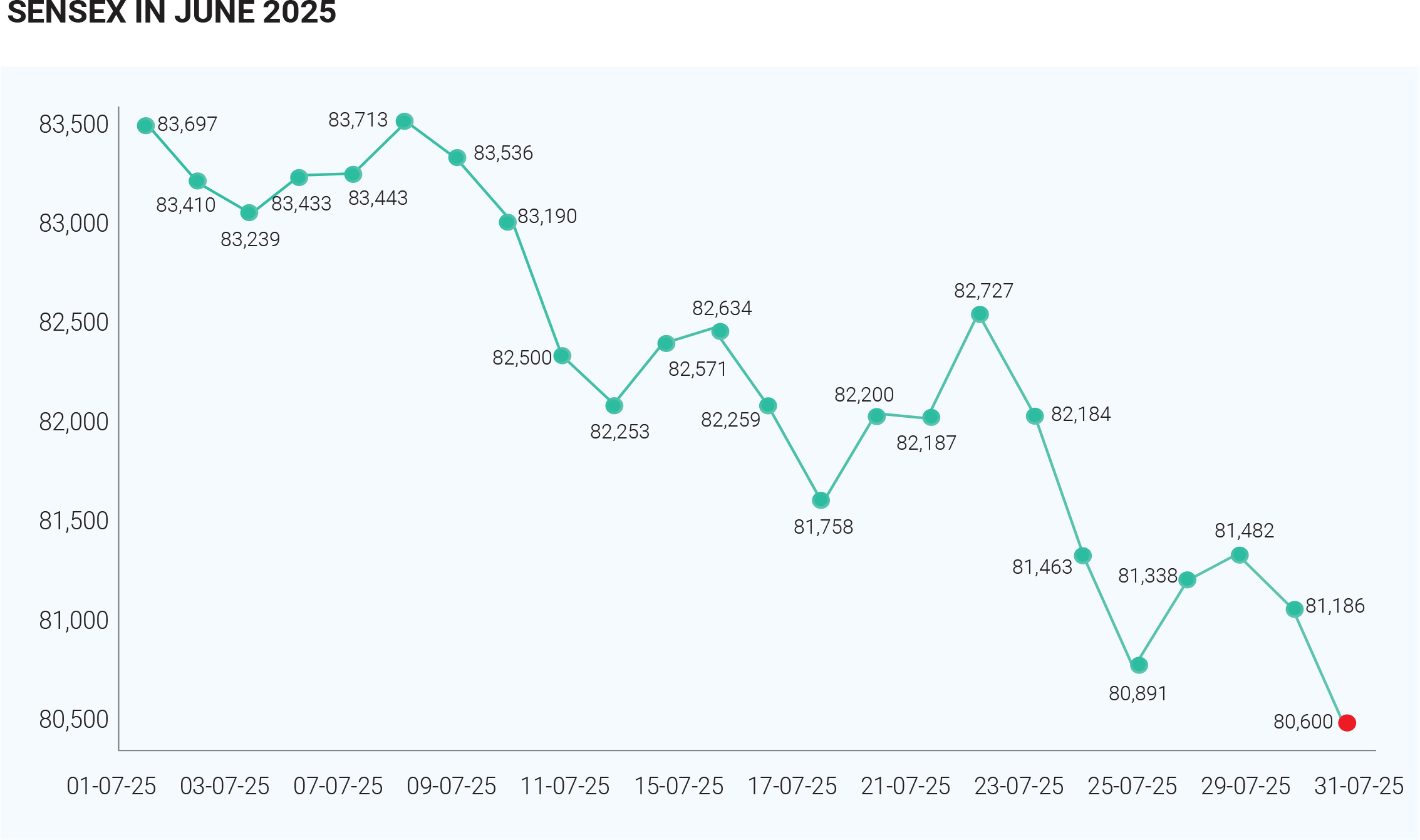

In July 2025, the Indian stock markets witnessed a largely negative trajectory, with the benchmark indices—Nifty 50 and Sensex—registering significant declines over the month. Market sentiment was consistently weighed down by a combination of global trade tensions, foreign fund outflows, mixed corporate earnings, and weakening investor confidence. The broader market mood remained cautious throughout, with periodic rebounds failing to arrest the overall downtrend. From the beginning of July, both the Sensex and Nifty displayed a clear downward trend. Although there were sessions marked by brief recoveries, these were often driven by short-covering or sectoral buying and lacked

the conviction needed to reverse the broader market weakness. The trend remained largely bearish across the month. On July 28, 2025, for instance, the Nifty closed at 24,680, down 0.63%, while the Sensex ended the day at 80,891, down 0.70%, underscoring the sustained weakness in the final trading days of the month. By the end of the month, the losses were evident. On July 31, 2025, the Nifty 50 closed at 24,768.35, down 86.70 points or 0.35% for the day, while the Sensex settled at 81,185.58, declining 296.28 points or 0.36%. Compared to their June closing levels, both indices recorded notable declines, reflecting a consistent erosion of investor confidence throughout the month. The broader weakness in July 2025 can be attributed to several key macroeconomic and sector-specific developments. One of the most impactful was the announcement by the U.S. President of a sweeping 25% tariff on Indian exports. This protectionist move was perceived as a significant threat to India’s global trade competitiveness and triggered widespread selling, particularly in export-linked and cyclical sectors. The policy not only added to global trade tension but also rekindled investor fears of a potential trade war scenario. Adding to the woes was the relentless selling by Foreign Institutional Investors (FIIs), who withdrew over ₹28,500 crore from Indian equities in July. This marked one of the sharpest monthly capital outflows in recent times and significantly impacted market sentiment. While Domestic Institutional Investors (DIIs) stepped in with strong net buying to absorb some of the pressure, their efforts were insufficient to offset the scale of FII withdrawals. This persistent capital flight kept the indices under pressure across multiple sessions. Global cues further exacerbated the negative trend. Asian markets were generally volatile, impacted by concerns over weakening Chinese demand, geopolitical tensions, and an appreciating U.S. dollar. Uncertainty around U.S.-India trade negotiations and conflicting macroeconomic commentary from global financial institutions added to the prevailing risk aversion. Consequently, Indian investors, already grappling with domestic challenges, found little encouragement from the international front. On the domestic front, Q1 FY26 corporate earnings presented a mixed picture. While some sectors like FMCG managed to hold their ground, major cyclical segments such as IT, consumer durables, and auto posted underwhelming results. The negative surprises in these sectors deepened the market correction, as investors reassessed growth expectations. Realty stocks also lagged, facing headwinds from regulatory overhang and funding concerns. Sectoral divergence became a defining feature of July’s market behaviour. Defensive sectors such as FMCG, healthcare, and pharmaceuticals demonstrated resilience. These stocks benefitted from their stable earnings outlook and defensive nature amid rising uncertainty. On the other hand, metals, IT, real estate, auto, and consumer durables were among the worst performers, impacted by global demand concerns, poor earnings, and valuation pressures. Despite the negative backdrop, India’s manufacturing sector offered a rare bright spot. The HSBC India Manufacturing Purchasing Managers’ Index (PMI) climbed to 59.1 in July—its highest reading in 16 months. This pointed to strong underlying domestic demand and industrial momentum. However, even this positive data point was insufficient to lift market sentiment, as broader headwinds from trade tensions and capital market volatility overshadowed domestic resilience. IPO activity, however, remained a pocket of strength. The primary market showed encouraging signs, especially among smaller companies. Thirteen SME IPOs were launched during the month, several of which were oversubscribed, highlighting investor appetite for new listings even as broader markets declined. This enthusiasm suggested that liquidity was still available for select opportunities, although the trend was not strong enough to influence the larger market direction. July 2025 was a challenging month for the Indian stock markets. Both Nifty 50 and Sensex trended lower, reflecting the cumulative impact of global trade disruptions, significant FII outflows, weak earnings in key sectors, and volatile global cues. The announcement of U.S. tariffs on Indian exports acted as a primary drag, triggering a broader re-evaluation of India’s trade prospects and equity valuations. Although the IPO market and select regulatory measures provided glimmers of optimism, they were overshadowed by macroeconomic concerns and capital market pressures. Looking ahead, while domestic growth fundamentals remain intact, the near-term outlook will likely depend on the resolution of global trade issues, the trajectory of foreign fund flows, and clarity on corporate earnings momentum.